Most small bakeries lose somewhere between $40–120 weekly through till variance—not from theft, but from broken reconciliation processes that quietly compound over time.

The issue usually isn't dishonest staff or bad math. It's the disconnect between your POS system, physical cash counts, and the operational reality of running a bakery where flour-covered hands handle money, morning rushes create chaos, and a single register serves multiple functions throughout the day.

After building operational software for dozens of bakeries, the pattern is pretty consistent: shops with 1–3 employees struggle most with cash controls because everyone does everything. The person taking payment also boxes pastries, answers phones, and handles wholesale pickups. Traditional cash handling procedures designed for dedicated cashiers simply don't map onto how small bakeries actually run.

Why standard POS reconciliation fails in small bakeries

Your POS terminal tells one story. Your cash drawer tells another. The gap between them grows wider each shift, and tracking down discrepancies becomes near-impossible once you're more than a day behind.

Standard retail cash handling assumes dedicated cashier roles, clear shift boundaries, and time for proper counts. Small bakeries operate differently. You might have three people accessing the same drawer across overlapping shifts. Morning prep starts at 4 AM but the "official" shift begins when doors open at 7 AM. Wholesale customers pay cash for large orders while retail customers buy single croissants.

The complexity multiplies when you factor in:

-

Tips pulled from the register throughout the day

-

Petty cash mixed with sales revenue

-

Vendor payments made from the till

-

Change runs that don't get documented

-

Multiple payment types handled differently in your POS

Each variance has an operational root cause. A $20 shortage might trace back to incorrect change given during the morning rush, a wholesale payment not properly recorded, or tips distributed without documentation. Without proper tracking, these small leaks turn into steady drains.

Traditional reconciliation waits until end of day, when the trail has gone cold. By then, you're reconstructing what happened eight hours ago while exhausted staff just want to leave. The investigation becomes cursory—mark the variance, move on, hope tomorrow is better.

The hidden cost of poor cash controls

That daily $15–20 variance seems manageable until you calculate the annual impact. A bakery averaging $2,800 in daily revenue and losing 1.5% to till variance gives up over $15,000 yearly—enough to fund equipment upgrades or hire seasonal help.

Never miss a bake or delivery again.

Bakeryly helps you schedule, track, and manage every order effortlessly.

- Unified order tracking

- Real-time inventory alerts

- Staff shift management

No credit card required

Time waste adds up fast. Spending 20 minutes daily hunting for discrepancies equals 120+ hours annually. That's weeks of labor spent on detective work instead of production or customer service.

Staff morale erodes gradually. Nobody enjoys being suspected when money goes missing. Good employees leave when they feel untrusted. Handling cash without clear procedures creates low-level anxiety that adds up over time.

Decision-making suffers. When your cash position is unclear, you can't confidently make purchasing decisions, plan investments, or understand true daily performance.

Audit risks increase. Poor documentation creates tax headaches. Missing receipts, unexplained variances, and informal petty cash handling attract scrutiny during reviews.

The operational drag compounds over time. Staff develop workarounds that bypass proper procedures. Informal practices get embedded. What starts as minor variance grows into systematic revenue leakage.

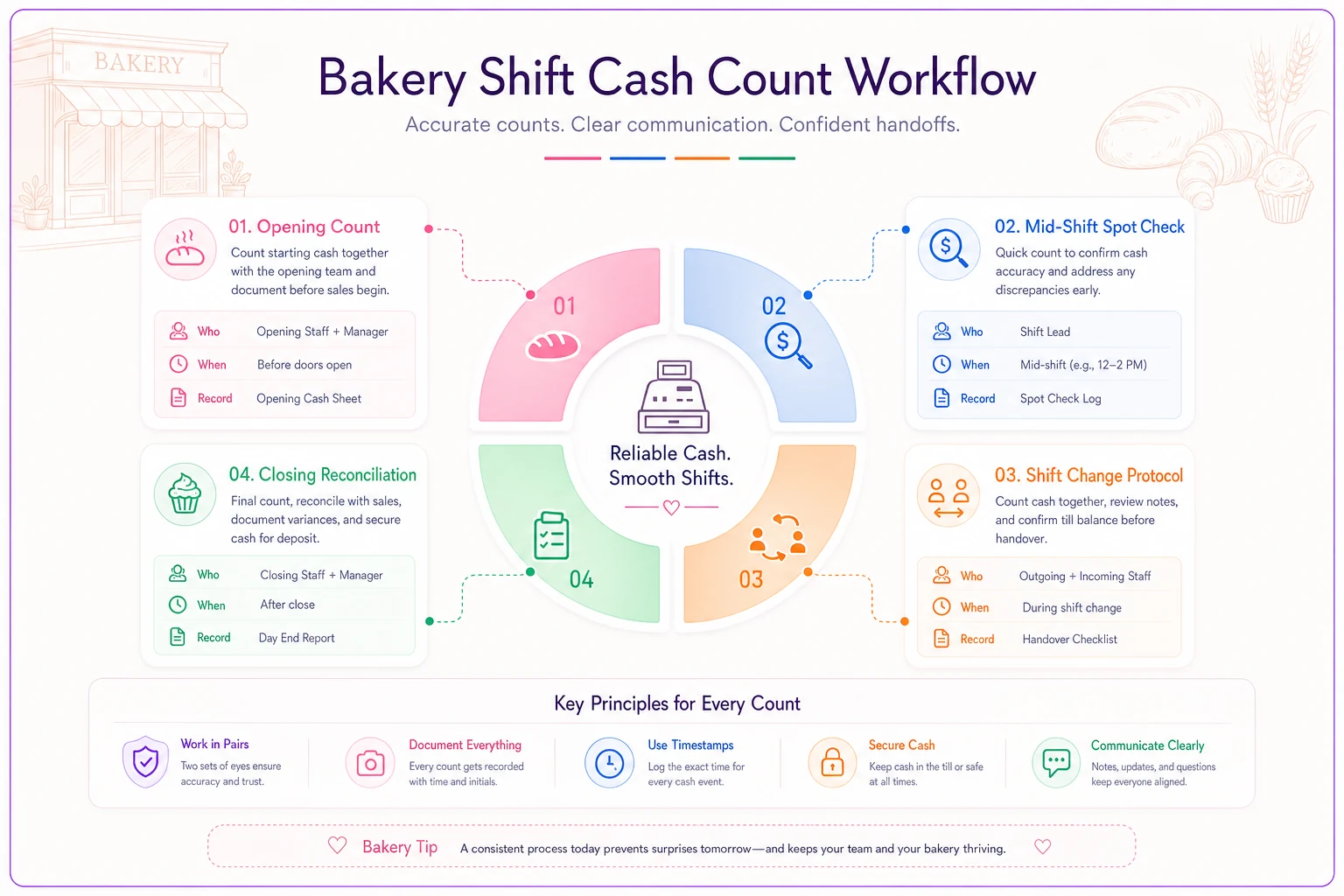

Building a shift cash count system that actually works

Effective bakery POS cash handling starts with shift-based controls, not daily reconciliation. When you catch variances within hours instead of days, investigation is straightforward.

Here's the shift count framework that works for small operations:

Opening Count (5 minutes) Count the drawer before any transactions. Document bills by denomination—don't just write "$200 float." Record: 10x$20, 15x$10, 20x$5, rolls of quarters/dimes/nickels/pennies. Take a phone photo as backup.

Note irregularities immediately. Damaged bills, foreign currency, or IOUs should be removed and documented before sales begin. This baseline prevents confusion later.

Mid-shift Spot Check (2 minutes) During slow periods, do a quick large bill count. Count twenties and above—ignore smaller denominations. Compare to POS cash sales. If variance exceeds $50, investigate while memories are still fresh.

This isn't a full reconciliation, just a sanity check. Train staff to do this naturally during downtime.

Shift Change Protocol (8 minutes) The outgoing person counts with the incoming person present. Both sign the count sheet. Any variance gets investigated before the first person leaves. Shared responsibility eliminates finger-pointing later.

Count everything: bills, coins, checks, gift certificates. Remove tips and document the amount. Pull any IOUs. The drawer should contain only business funds.

Closing Reconciliation (10 minutes) Match physical count to POS report. Document variances by category: over/short, by denomination if known. Note any unusual transactions—large cash sales, returns, voids.

Don't just record the variance number. Add context: "Short $18—busy morning rush 7–9 AM, Jane training new staff, two voids for wrong orders." That information proves invaluable when patterns emerge.

This flow highlights who does each count and when, making it easy to follow during service.

Count twenties and above during mid-shift spot checks to save time.

This isn't a full reconciliation, just a sanity check. Train staff to do this naturally during downtime.

Variance investigation that finds root causes, not scapegoats

When till variance occurs, most bakeries either ignore it or conduct fruitless witch hunts. Neither works. You need systematic investigation that identifies operational causes without creating an accusatory environment.

Treat variance as process failure, not people failure. Your investigation should uncover where procedures break down.

For overages (drawer has more than POS shows): Start with untendered transactions. Did someone pay cash but the sale wasn't rung up? Check for handwritten orders that bypassed POS. Review wholesale payments—these often get handled outside normal procedures.

Look for reversed transactions. Voids or returns might be recorded twice. Credit card tips sometimes get counted as cash. Gift certificate redemptions can create phantom overages if handled incorrectly.

For shortages (drawer has less than POS shows): Review large transactions first. A $50 shortage often traces to one mistake rather than multiple small errors. Check bills—did someone give $30 change for a twenty?

Examine mixed payment sales. When customers pay partially in cash and card, errors multiply. The POS might show full cash payment when half went on card.

Investigate non-sales withdrawals. Tips taken, vendor payments, or change runs often create shortages when not properly documented. Check whether petty cash got mixed with sales revenue.

Pattern recognition over time:

-

Day of week (Saturdays often show more variance due to volume)

-

Shift timing (morning rush vs. afternoon lull)

-

Staff combinations (some pairings work better together)

-

Transaction types (wholesale vs. retail)

After a couple of weeks, patterns usually emerge. Maybe Tuesday afternoons consistently run short because that's when supply vendors get paid from the till. Maybe new staff need better training on gift certificate processing.

Petty cash rules that prevent till contamination

Mixing petty cash with sales revenue creates reconciliation nightmares. Small bakeries need petty cash for emergency supplies, tips, and minor expenses—but it shouldn't live in your register.

Establish a separate petty cash fund of $100–150. Keep it in a locked box in the back, not the register. Physical separation prevents accidental mixing and simplifies tracking.

Approved petty cash uses:

-

Emergency supplies under $25 (milk, eggs when delivery fails)

-

Parking for delivery vehicles

-

Small equipment repairs

-

Postage and shipping

-

Tips and gratuities for service vendors

Require documentation for everything: Every withdrawal needs a receipt or signed note. No exceptions. "Borrowed $20 for milk—Sarah" doesn't cut it. Include: date, amount, purpose, vendor, who approved it, and attach the store receipt.

A simple log sheet works fine:

| Date | Amount | Purpose | Vendor | Approved By | Receipt? |

|---|---|---|---|---|---|

| 10/15 | $18.50 | Emergency butter | Corner Store | Tom | Yes |

| 10/16 | $5.00 | Parking meter | City | Sarah | No |

Weekly reconciliation: Count petty cash every Monday morning. The fund plus receipts should equal your starting amount. Replenish from the register only after completing sales reconciliation. Document the transfer clearly in both records.

If petty cash runs low mid-week, that's a planning problem. Don't pull from the register—it creates variance you'll struggle to trace. Better to delay non-critical purchases than contaminate your sales revenue.

Never use petty cash for:

-

Salary advances or personal loans

-

Bill payments or utilities

-

Major supply purchases

-

Change fund replenishment

These restrictions seem rigid, but they prevent the gradual slide into chaos. Once exceptions start, petty cash becomes a slush fund that complicates every reconciliation.

A lightweight weekly audit for 1–3 person bakeries

Traditional audits assume dedicated back-office staff and extensive documentation. Small bakeries need lightweight checks that catch problems without disrupting operations.

This roughly 20-minute weekly audit catches most issues before they compound.

Monday Morning Cash Position Review (5 minutes) Compare last week's daily variances. Look for total weekly variance exceeding 0.5% of cash sales, any single day over $30, and patterns in timing or staff. Calculate your variance run rate—average daily variance times 365. If that number exceeds $3,000 annually, you have a systematic problem that needs attention now.

Transaction Spot Checks (7 minutes) Pull five random cash transactions from last week. Verify the amount in POS matches the receipt, that correct change would have been given, that voids or modifications are explained, and that the timeline makes sense. Focus on cash transactions over $50—mistakes here hit reconciliation harder.

Deposit Verification (3 minutes) Match POS cash reports to bank deposits. The path should be clear: Thursday's cash sales → Friday's deposit slip → Monday's bank statement. Any gaps indicate process breakdown. Check deposit timing too—holding cash too long increases loss risk and makes investigation harder.

Inventory Quick Count (5 minutes) Count five high-value items—specialty cakes, wholesale orders. Compare physical count to POS sales. Discrepancies might indicate unrecorded cash sales or theft. This isn't full inventory management, just a spot check for obvious issues. If your POS shows you sold eight croissants but you made three dozen and only have four left, investigate.

Documentation Review Confirm all required paperwork exists: shift count sheets for each day, variance explanations when over $10, petty cash receipts and log, and void/return documentation. Missing paperwork signals process breakdown. Better to catch it weekly than discover gaps months later during tax prep.

Technology helps, but process comes first

Modern POS systems offer cash management features—automated reporting, variance tracking, anomaly detection. But technology can't fix broken processes. The fanciest POS won't help if staff bypass procedures or documentation stays sporadic.

Start with process discipline. Once basic procedures work consistently, technology amplifies their effectiveness. Building reliable operational workflows always beats hoping software solves human problems.

That said, the right tools do make a difference. Look for POS features that support your workflow:

Forced cash counts: Systems that require drawer counts at shift changes prevent skipping this critical step. The POS won't allow new transactions until counts are complete.

Variance flagging: Automatic alerts when variance exceeds thresholds—like $20 or 1% of sales—prompt immediate investigation while details are still fresh.

Blind counts: Staff enter their count before seeing the expected amount. This prevents backing into the right number and surfaces true discrepancies.

Audit trails: Complete logs of every modification, void, discount, and return with timestamp and employee ID. When investigating variance, these details matter.

A bakery running Excel sheets with disciplined procedures beats one with expensive POS systems and sloppy execution every time.

When cash handling problems signal something deeper

Persistent till variance often points to broader operational problems. The cash discrepancies you're seeing are symptoms.

High variance during rushes suggests understaffing or poor training. When people feel rushed, mistakes multiply—wrong change, forgotten ring-ups, incorrect transaction processing. The solution isn't more cash controls; it's better staffing and workflow design.

Variance concentrated around specific products might reveal pricing confusion. If your POS has old prices but shelf tags show new ones, staff make manual adjustments that create discrepancies. Regular price audits prevent this drift.

Wholesale cash handling deserves special attention. Large cash payments, informal invoicing, and delivery timing create perfect conditions for variance. These transactions need their own procedures—separate documentation, dual verification, immediate POS entry.

Cash handling also intersects with other systems. Your KPI tracking setup should include variance metrics. Production planning affects transaction complexity. Customer flow affects error rates.

The goal isn't eliminating variance entirely—some amount is inevitable. But variance consistently exceeding 0.5% of cash sales means something systematic needs to be fixed.

What actually happened at one Denver bakery

A small bakery in Denver was dealing with daily variances averaging $35–40. The owner suspected theft but couldn't prove anything. Staff morale dropped as suspicions grew.

After implementing structured procedures, the first week revealed the actual problem: no theft—just broken processes. Wholesale customers paid cash for large orders that got recorded hours later. Tips were pulled randomly without documentation. The morning baker made change from the previous day's deposit bag.

New procedures took about two weeks to stick. Separate wholesale payment documentation. Locked deposit bags. A tip envelope system. Forced counts at every shift change.

After one month, the results were pretty clear:

-

Average daily variance dropped to $8–12

-

Weekly audit time went from roughly 2 hours to about 20 minutes

-

Staff stress visibly decreased

-

The owner stopped cash firefighting and started focusing on growth

The unexpected discovery: actual cash sales were around 8% higher than the POS showed. Unrecorded transactions—especially wholesale—had been hiding true performance. Fixing cash handling surfaced over $1,100 weekly in previously invisible revenue.

Making the system stick

Perfect procedures fail without consistent execution. Limited staff means everyone must understand and follow cash protocols.

Start with the highest-impact changes. Implementing forced shift counts alone reduces variance by 30–40% for most bakeries. Add variance investigation and you'll catch the majority of issues. Perfect documentation can come once the basics work.

Train through practice, not theory. Do mock counts together. Walk through variance investigations. Role-play difficult situations—customer disputes, large bills, mixed payments. Hands-on training sticks better than written procedures.

Create visible reminders. Laminate count sheets and investigation scripts. Post till variance targets where staff see them. Display the weekly variance trend—visual feedback drives improvement.

Build accountability without blame. Variance happens to everyone. Focus on learning and improvement, not punishment. When someone catches their own mistake through proper counting, that's the system working exactly as intended.

Most importantly: stay consistent. Skipping counts during busy periods or letting documentation slide creates gaps that compound. Simplified counts done consistently beat perfect counts done occasionally.

Proper bakery POS cash handling isn't about catching thieves—it's about building operational discipline. When cash handling runs smoothly, you gain confidence in your numbers, reduce staff stress, and free up mental energy for what actually matters: making great products and serving customers well.

Pick one improvement—shift counts, variance tracking, petty cash separation—and start tomorrow. Build from there. Within a month, you'll wonder how you operated without it.

Ready to elevate your bakery operations?

Join 2,000+ bakeries using Bakeryly to streamline workflows, reduce waste, and delight more customers.